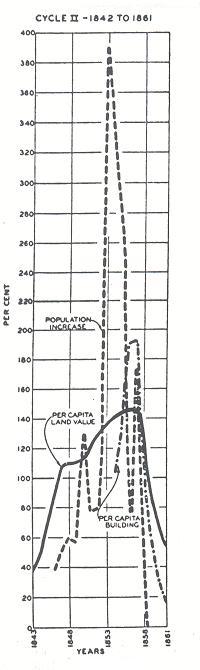

Clearing-house procedures are of interest to us because details of its operations are available to study, as are the statements banks had to issue, to comply with clearing-house regulations. Clearing-house records reveal the rise and fall of New York banking credit, i.e. banks loans, deposits and specie on hand.

J S Gibbons, in his work The Banks of New York, Their Dealers, The Clearing House, and The Panic of 1857, gives clearing house figures for 1854 to 1858, and it is from these statistics, and the book itself, that the following analysis is drawn. If Gibbons' work can be believed, and there is no reason to doubt it though a second source would be useful to confirm his clearing-house figures, we can say that the 1857 October panic was a direct result of banks curtailing credit operations after the August collapse of the Ohio. But we are slightly ahead of ourselves. In the clearing-house figures, one may notice a seasonality of loan contraction each year around August. Loans reached their highest point of expansion in the first week of August for 1853 and 1854, the third week of August in 1855, and once again in the first week of August for 1856. This was not co-incidental, and there was believed to be good reason for it (though this may not have been so obvious to market participants at the time): it was the by-product of an agricultural economy, which America still was at this time. Ron Insana, Trendwatching, page 167, noted it this way: "…the harvest period was one of notable volatility both in market terms and in terms of liquidity or money available in the nation's banks. As the harvest neared, farmers routinely pulled their money out of big-city banks to finance the labour needed to harvest crops. That put a drain on available cash in the nation's money centers. Stock prices typically fell from August to October, owing to the lack of available funds. But stock prices bottomed in October when farmers, flush with cash from the sale of their crops, re-deposited the proceeds in the New York banks." Insana goes on to point out that some market experts believe this to be the principal reason why the stock market has had a historic tendency to crash and bottom out in the month of October. The August loan contraction would then proceed mostly in an orderly fashion till about mid November. Smith and Cole also noted this seasonal loan contraction, page 127. (Sometimes there was another small decline in late March / early April.) Rail statistics bear out this phenomenon. Rail employment tended to rise sharply in the autumn when the carrying of agricultural produce reached its peak. Employment then declined into the winter months. (See for example Walter Licht, Working for the Railroad.) So rail companies would have added to the currency requirements at this time in order to pay workers, a fact which could only have gotten more pronounced over coming decades.

In the four years of data here, the largest decline prior to October 1857 took place 36 months prior, in October of 1854. For the year 1857, credit contraction began August 8, continuing in the normal seasonal manner for the next two weeks. There were a couple of reports of company failures and one larger misuse of funds in a leading rail company in these weeks, but it was not considered too much out of the ordinary.

The Ohio bank failure of the 24th August was not of itself considered immediate cause for concern, the main branch in Cincinnati was after all reported (by telegraph) to be open for business as usual. However shortly thereafter it was discovered that practically the entire capital base of the bank had been embezzled - some 2 million dollars. Most New York banks were creditors of the Ohio. Suddenly New York merchants found their banks a little less accommodating in their credit. The next week's clearing-house report confirms the course of banking policy to have changed substantially. Credit was contracting. "The most violent (bank) action was between September 5th and September 19th, when the loans were reduced $3,443,944 in the face of an increase in deposits of nearly six hundred thousand dollars… There can be no escape from these figures. They show beyond (doubt), that the banks, not the depositors, took the lead in forcing liquidation." (Gibbons, page 354.) A credit squeeze initiated by the banks, to restore their balance sheets. Up to the 26th September, depositors had not been alarmed. Only after October 3rd, for some reason, was the trust of depositors reversed. Clearing house data suggests the panic was a direct result of the marked contraction of credit by the banks after the 24th August. Note though, the possibility for panic could not have been set up without the substantial lift in bank credit in the four years prior to 1857. Said Gibbons, page 346: "Such is the outline of the most extraordinary, violent, and destructive financial panic ever experienced in this country."

Until the next one, 17 years later in 1873.

The scams.

It remained only for the scams, cons and frauds to come to light. And more than a few persons, at more than a few companies it seems, were discovered with their hands deep in the till. Fraud was found at the Ohio bank, as you would expect, embezzlement by the cashier, (to sustain his stock market operations apparently, says Kindleberger, I, page 71) in addition to the banks souring investments in highly speculative railroad bonds.

In another case in New York, Robert Schuyler (a grandson of Alexander Hamilton's nephew) president of both the Harlem, and New Haven railroads, was found to have secretly printed twenty thousand shares of New Haven stock and sold it, quietly, on market. By the time of the discovery, Schulyer was already well and truly on his way to the nearest border - Canada - with proceeds of about $2 million. He was never caught.

An assailant of Schulyer and secretary of the Harlem Railroad, Alexander Kyle Jr., admitted to having forged some five thousand shares of Harlem stock and swapped them for securities in the New Haven line, which were also forgeries. Kyle Jr. had had a hand in picking an apartment for Schulyer's mistress, though the discovery of this was nothing as to when the New York social set found out Schulyer had been leading a double life and fathered a second family under the assumed name of Spicer. (Sobel page 90.) Not to be outdone, the Board of Directors of Parker Vein Coal Company were found to have issued five times as much stock as had been authorized and gone on to sell it, pocketing the proceeds. A teller at the Ocean bank paid himself out some $50,000 of the banks funds, a teller at the National grabbed $70,000. The bookkeeper of the Union Bank stole $200,000 and promptly fled with the loot after it was discovered he had been forging balances for months.

The Bank of Sandstone, it was later discovered, never had any specie, and never had any assets to cover its liabilities at the time of it being reported upon by the commissioners of Michigan State. The Exchange Bank of Shiawasee was found by the same commissioners to have a mere seven coppers and small amount of paper in its vaults, whilst it had bills in circulation of $22,267. The Jackson County Bank was discovered to have many large and full boxes in its own vaults, but whilst the tops of each showed silver dollars, they covered little else but nails and glass. (Lightner, History of Business Depressions, chapter XIV.)

That Blizzard.

The winter of 1856/57 had already been noted for its more brutal cold than usual, though also for a general lack of snow. On Jan 16th through 19th 1857, the east coast was struck by a 'monster blizzard' that would be long remembered for its intensity and howling winds. The weekend of the 17th and 18th was particularly extreme; record winds and temperatures as low as 20 degrees below zero (Fahrenheit) recorded in some parts. Interestingly, warmer weather followed, with a further change in conditions to severe cold following on Jan 23, known as cold Friday, and then even colder Jan 24th, with a low of -55 recorded in northern New England. (Typical extremes on Gann dates.) A great description of events is on the web at geocities.com/donsutherland1/1857blizzard2.html

Robert Sobel, in his book Panic on Wall Street: A History of America's Financial Disasters, lists the Western blizzard of 1857 as one of the 12 most harrowing moments in American financial history from 1792 to 1962. In one review of the book, it was noted that Sobel chose these particular (12) cases, among a dozen or so others, to demonstrate the complexity and array of settings that have led to financial panics, and to show that we can only make the vaguest generalizations about panic as a phenomenon. Well I hope you can see through such an argument. There does not have to be land and real estate speculation to bring on a panic of course; however if real estate is involved, the collapse will be worse, more prolonged, and harder to get out of than otherwise would be the case. (With a downturn rythym of about every 18 to 20 years it would seem) There is an order amidst the chaos of boom and bust, and liberal credit is ALWAYS at the heart of it. But economic collapse requires something else as well. Feb 21 1854 had also seen great storms hit the east coast, "The most tremendous snow storm ever known here commenced last night," said the Feb 22 issue of the New York Daily Times. But no panic followed; the economic sandcastle had not yet been built high enough to enable that 'un-looked for' event to shatter public confidence.

Some after effects of the downturn:

The downturn was yet another development that gave the 'South' further reason for despising the North (slavery was the big issue) and helped deepen the divide that brought on the US civil war (1861). The downturn in the South ended up not as severe as in the north, owing to the fact this time that cotton exports held up relatively well. To the South, the wealth of the country was in farming, not in reckless 'land and stock jobbing'. Southerners now genuinely believed their economic welfare really was at the mercy of northern bankers and their reckless speculations. Funny how war has often followed an economic downturn…

As might be expected, the newspapers of the day expounded all sorts of reasons for the decline in economic activity (see below) and a new-found era of self-criticism dawned. "The puzzling question repeatedly asked was how a country with a rapidly growing population, rich in fertile soils and natural resources, producing food in abundance, busily engaged in manufacturing and commerce, could get itself into such a predicament." (Stampp page 231.) Indeed. "It seems indeed very strange," wrote another bewildered observer, "that in the very midst of apparent health and strength…the whole country…should suddenly come to a dead stop and be unable to move a step forward - and that we should suddenly wake up from our dreams of wealth and happiness, and find ourselves poor and bankrupt." (Nashville Republican Banner, October 18, 1857, quoted by Stampp page 231.)

The answer of course is 'your standing on it', but this would have to wait another two cycles, and the writings of Henry George, (which shook the US to its foundations), to prove it.

Some relevant items out of books, that I found of further interest:

The Stock Market Barometer, William Peter Harrison, quoting Charles Dow: "The panic in Europe in 1847 exerted but little influence in this country (USA), although there was a serious loss in specie, and the Mexican war had some effect in checking enterprise. These effects, however, were neutralized somewhat by large exports of bread-stuffs and later by the discovery of gold in 1848-9...There was a panic of the first magnitude in 1857, following the failure of the Ohio Life Insurance and Trust Company in August. This panic came unexpectedly, although prices had been falling for some months. There had been very large railroad building, and the proportion of specie held by banks was very low in proportion to their loans and deposits. One of the features of this period was the great number of failures. The banks generally suspended payments in October."

Summarizing Charles Kindleberger, Mania's, Panics and Crashes, about 1857:

Probably the first truly worldwide felt (panic and) downturn. Gold discoveries in California 1849 and in Australia 1851 vastly increase the credit / money base of the US and some parts of Europe, especially Britain, feeding the existing railroad and banking booms, the banks in particular lending vast sums to further finance trade and industry. Speculation runs rampant; US, railroads and public lands, UK, railroads and wheat, on the Continent in railroads and heavy industry. Speculative peak, US and England end of 1856,

Panic August 1857 in the US, October 1857 in the UK. Speculative peak on the continent, March 1857, panic November. The collapse was made worse following the ending of the Crimean war and subsequent collapse of wheat prices. War financing had fed the huge expansion of credit in the first place. At the peak, UK banks had lifted interest rates to 12-15%. In the downturn, few banks could be found to honour or accept any bills of exchange whatsoever.

Alfred Chandler, Land Title Origins (page 491) made an important observation of his era: "With each recurring land boom there has been a new crop of speculators, with similar endings in each succeeding panic - occurring about every twenty years. But land values on the crest of every land boom are always higher than they were on the crest of the preceding boom - and that is the backlog which keeps the fires of land speculation for ever going." Chandler noted further (on page 499): "Huge sales of land from the public domain to speculators, on credit, just previous to 1857, brought on another financial crisis, as similar speculation had brought on previous panics and years of depression…There followed in the same pattern the panics of 1819 and 1837, and this one, which began with the failure of the Ohio life and Trust Company. Millions of dollars of its depositors and policy-holders money had been loaned by it to holders of idle land, and to promoters, to build railroads through unproductive regions and to attract buyers of land."

And some quotes:

Ebullience at the top:

"Cincinnati presented to the world a picture of progress heretofore unknown to the history of cities. Its solidity and continued prosperity had become matters of special wonder."

Cincinnati Enquirer, June 3 1857 (quoted also in Stampp, page 213.)

Then the fear:

"It is a gloomy moment in history. Not for many years - not in the lifetime of most men who read this paper - has their been so much grave and deep apprehension; never has the future seemed so incalculable as at this time. In our own country there is universal commercial prostration and panic, and thousands of our poorest fellow citizens are turned out against the approaching winter without employment, and without the prospect of it. In France the political cauldron seethes and bubbles with uncertainty; Russia hangs, as usual, like a cloud, dark and silent upon the horizon of Europe; while all the energies, resources and infancies of the British Empire are sorely tried, and are yet to be tried more sorely."

Harpers Weekly, vol. I, page 642, Oct 10 1857

"All the panics previously experienced are as nothing compared with that of today. If there is a much lower depth for some stocks, they will go completely out of sight."

New York Herald, Oct 3 1857

"Several of the clergy preached hard times sermons yesterday enjoining patience under adversity. The parsons might well have preached to the winds. Money is the thing that is wanted - money ! money ! money! - not homilies from the book of job."

Newark Daily Advertiser, Oct 7 1857.

"The financial condition of our country is unprecedented. Business of all kinds is more completely suspended than if a hostile fleet had anchored in our harbor."

New York Evening Post, Oct 9 1857

"Like a star of the night, darting out of the skies and losing itself in the sea, the whole country has suddenly, and while in the enjoyment of unparalleled prosperity, plunged headlong down into universal bankruptcy. Now no one is any longer known to be rich."

New York Evening Post, Oct 14, 1857

Blame the government:

"Had we had more statesmen and fewer politicians, the country would not have been reduced to its present distressing and humiliating condition."

Philadelphia Pennsylvanian, Sept 12, 1857

"The Democratic Party is responsible for all these troubles…"

North American and United States Gazette, Philadelphia, Sept 24 1857

Blame anything, except the speculation in government granted licenses and privileges:

"Men speak of overstocking the market, or of over manufacturing, or overimportations, and of extravagance of various kinds."

The Independent, Oct 8 1857

The great men of the exchange, to whom we bowed with a selfish idolatry, are proving to be but wooden images."

Leavenworth City Herald (Kansas) Oct 17 1857

"The cause of our present (distress is) that our dry goods merchants have over imported…"

Letter to the editor, Newark Daily Advertiser, Sept 25 1857

"Our present disorders have been provoked by the extravagance of our women. Crinoline and moiré, gloves and feathers, fans and furbelows, kickshaws and gewgaws, these have ruined us. These have drained us of our western wheat and our Californian gold, to give us in return only hotel flirtations and watering place polkas."

New York Weekly Times, Oct 17 1857

"What caused trade thus to topple over, almost without a struggle ? What hurled to the dust so many stately fabrics of industry, skill and enterprise ? The answer is plain enough - we have been living too fast."

Philadelphia Press, Oct 12 1857.

I listed one of the causes as the telegraph, disseminating the bad news, as it was, 'too quickly'.

And finally:

The I lays it to wine, women, cards and (wait for it) fast horses."

Washington Evening Star, Aug 28 1857 I